Photovoltaic Market Share Analysis and Growth Drivers Forecast 2035

https://www.marketresearchfuture.com/reports/photovoltaic-market-1061

As per Market Research Future, the Photovoltaic Market Share

is expanding significantly as global economies accelerate the transition toward renewable energy sources. Photovoltaic (PV) technology, which converts sunlight directly into electricity using semiconductor materials, has become one of the most widely adopted clean energy solutions worldwide. Increasing climate concerns, supportive government policies, and declining solar panel costs are major factors influencing the competitive landscape and distribution of market share among key players.

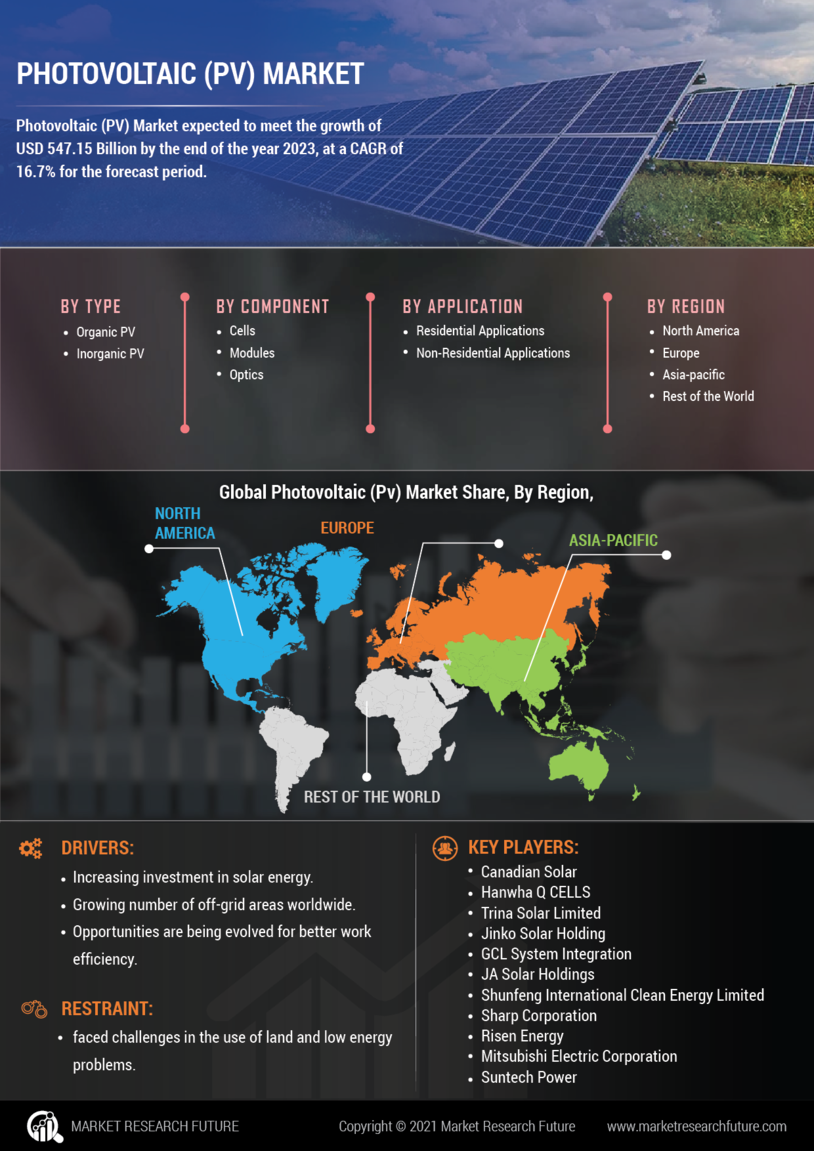

The global photovoltaic market share is largely dominated by Asia-Pacific, with countries such as China, India, Japan, and South Korea leading in both manufacturing capacity and solar installations. China, in particular, holds a substantial share due to its large-scale production facilities, government incentives, and massive deployment of solar farms. North America and Europe also maintain strong market positions, driven by renewable portfolio standards, tax incentives, and ambitious carbon neutrality targets.

In terms of technology segmentation, crystalline silicon solar panels command the largest share of the photovoltaic market. Monocrystalline panels are especially popular due to their high efficiency and long operational lifespan. Polycrystalline panels also contribute significantly, particularly in cost-sensitive projects. Thin-film technologies, while holding a smaller share, are gaining attention for their flexibility, lightweight properties, and suitability for specialized applications such as building-integrated photovoltaics (BIPV).

The utility-scale segment accounts for a considerable portion of overall market share. Large solar farms installed to supply power to national grids represent a major contributor to revenue generation. However, the residential and commercial segments are rapidly increasing their share, supported by rooftop solar adoption, net metering policies, and distributed energy generation trends. The rising popularity of solar-plus-storage systems is further reshaping the market share distribution across segments.

Competitive strategies among key market participants are centered on innovation, cost optimization, and vertical integration. Leading manufacturers are investing in research and development to enhance cell efficiency, reduce degradation rates, and improve energy yield. Strategic partnerships, mergers, and acquisitions are common, enabling companies to strengthen supply chains and expand global footprints.

Another important factor influencing photovoltaic market share is the increasing emphasis on sustainability and environmental responsibility. Companies adopting eco-friendly manufacturing practices and recycling programs are gaining competitive advantages. Additionally, advancements in digital monitoring and smart inverters are enhancing system performance, making photovoltaic installations more reliable and efficient.

As global electricity demand continues to rise and governments implement stricter emissions regulations, the photovoltaic market share is expected to evolve further. Emerging markets in Latin America, the Middle East, and Africa are presenting new opportunities for growth, potentially reshaping the global competitive landscape in the coming years.

FAQs

1. Which region holds the largest photovoltaic market share?

Asia-Pacific holds the largest share, primarily due to strong manufacturing capacity and extensive solar installations in countries like China and India.

2. What technology dominates the photovoltaic market?

Crystalline silicon technology, especially monocrystalline panels, dominates due to high efficiency and durability.

3. How does utility-scale solar impact market share?

Utility-scale solar projects contribute significantly to total revenue, making them a major segment in the photovoltaic market.

Photovoltaic Market Share Analysis and Growth Drivers Forecast 2035

https://www.marketresearchfuture.com/reports/photovoltaic-market-1061

As per Market Research Future, the Photovoltaic Market Share

is expanding significantly as global economies accelerate the transition toward renewable energy sources. Photovoltaic (PV) technology, which converts sunlight directly into electricity using semiconductor materials, has become one of the most widely adopted clean energy solutions worldwide. Increasing climate concerns, supportive government policies, and declining solar panel costs are major factors influencing the competitive landscape and distribution of market share among key players.

The global photovoltaic market share is largely dominated by Asia-Pacific, with countries such as China, India, Japan, and South Korea leading in both manufacturing capacity and solar installations. China, in particular, holds a substantial share due to its large-scale production facilities, government incentives, and massive deployment of solar farms. North America and Europe also maintain strong market positions, driven by renewable portfolio standards, tax incentives, and ambitious carbon neutrality targets.

In terms of technology segmentation, crystalline silicon solar panels command the largest share of the photovoltaic market. Monocrystalline panels are especially popular due to their high efficiency and long operational lifespan. Polycrystalline panels also contribute significantly, particularly in cost-sensitive projects. Thin-film technologies, while holding a smaller share, are gaining attention for their flexibility, lightweight properties, and suitability for specialized applications such as building-integrated photovoltaics (BIPV).

The utility-scale segment accounts for a considerable portion of overall market share. Large solar farms installed to supply power to national grids represent a major contributor to revenue generation. However, the residential and commercial segments are rapidly increasing their share, supported by rooftop solar adoption, net metering policies, and distributed energy generation trends. The rising popularity of solar-plus-storage systems is further reshaping the market share distribution across segments.

Competitive strategies among key market participants are centered on innovation, cost optimization, and vertical integration. Leading manufacturers are investing in research and development to enhance cell efficiency, reduce degradation rates, and improve energy yield. Strategic partnerships, mergers, and acquisitions are common, enabling companies to strengthen supply chains and expand global footprints.

Another important factor influencing photovoltaic market share is the increasing emphasis on sustainability and environmental responsibility. Companies adopting eco-friendly manufacturing practices and recycling programs are gaining competitive advantages. Additionally, advancements in digital monitoring and smart inverters are enhancing system performance, making photovoltaic installations more reliable and efficient.

As global electricity demand continues to rise and governments implement stricter emissions regulations, the photovoltaic market share is expected to evolve further. Emerging markets in Latin America, the Middle East, and Africa are presenting new opportunities for growth, potentially reshaping the global competitive landscape in the coming years.

FAQs

1. Which region holds the largest photovoltaic market share?

Asia-Pacific holds the largest share, primarily due to strong manufacturing capacity and extensive solar installations in countries like China and India.

2. What technology dominates the photovoltaic market?

Crystalline silicon technology, especially monocrystalline panels, dominates due to high efficiency and durability.

3. How does utility-scale solar impact market share?

Utility-scale solar projects contribute significantly to total revenue, making them a major segment in the photovoltaic market.